2026 Outlook - How AI Will Redefine Cross-Border B2B Payments and the Customer-to-Cash Journey

AI moves from optimization to autonomous orchestration across the entire customer-to-cash lifecycle

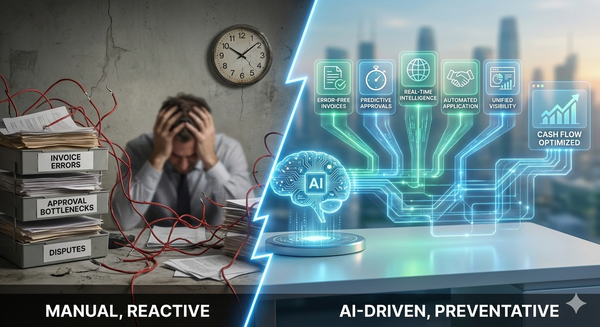

If 2025 was the year AI became foundational to cross-border payments, 2026 will be the year it becomes autonomous, predictive, and deeply embedded across the entire customer-to-cash journey. What today feels like optimization will evolve into orchestration - where AI continuously aligns payments, credit, risk, invoicing, and cash application in real time.

For CFOs and finance leaders, this shift will fundamentally change how global revenue is protected, accelerated, and scaled.

From Optimization to Autonomous Cross-Border Payment Decisioning

In 2026, cross-border payment optimization will move beyond human-defined strategies. AI will no longer just recommend actions - it will execute them within predefined guardrails.

AI systems will autonomously:

• Select optimal payment rails by corridor, currency, and counterparty

• Balance speed, cost, FX exposure, and risk in real time

• Adjust execution strategies dynamically as conditions change

This marks a transition from AI-assisted finance teams to AI-led payment decisioning, redefining what best-in-class cross-border payments look like.

Payments Become a Native Layer of the Customer-to-Cash Journey

Today, payments are often treated as a downstream step. In 2026, AI will pull payments upstream, embedding them directly into the customer-to-cash lifecycle.

AI will connect:

• Customer onboarding and credit assessment

• Invoice issuance and payment method selection

• Cross-border payment execution and reconciliation

• Cash application and dispute resolution

This convergence means payment behavior will directly influence credit terms, collection strategies, and customer experience in real time. The result is a faster, more resilient, and more intelligent customer-to-cash journey.

Predictive Credit and Risk Across Borders

Cross-border B2B transactions carry layered risk - FX volatility, counterparty reliability, regulatory exposure, and dispute probability. In 2026, AI will unify these signals.

Advanced models will:

• Predict late payments before invoices are issued

• Adjust credit limits dynamically by market and customer

• Influence payment routing based on dispute and chargeback likelihood

• Continuously refine risk scores using payment outcomes

Rather than reacting to issues, finance teams will prevent them. This predictive layer will be a defining feature of next-generation B2B cross border payment solutions.

Hyper-Scalable Bulk and Batch Payments Cross Border

As global platforms grow, bulk payments cross border will continue to rise sharply in volume and complexity. In 2026, AI will fully orchestrate these flows.

AI-powered systems will:

• Automatically construct and optimize cross border batch payments

• Split or merge batch payments cross border based on liquidity, cut-off times, and FX conditions

• Detect anomalies within cross border bulk payments before execution

• Self-heal failed transactions without manual intervention

This level of intelligence will allow companies to scale internationally without scaling operational headcount.

For a dedicated deep-dive into batch payments, see Batch Payments Cross Border: The Missing Link in Scalable Global Customer-to-Cash.

Multi-Currency Intelligence Becomes Strategic

By 2026, cross border multi currency payment capabilities will move from operational necessity to strategic advantage.

AI will:

• Forecast currency exposure weeks or months ahead

• Recommend optimal invoicing currencies by customer segment

• Net receivables and payables across multi currency payment cross border flows

• Optimize FX execution timing automatically

Currency will no longer be a passive cost - it will become an actively managed lever within the customer-to-cash strategy.

End-to-End Cross Border Payment Automation Without Loss of Control

Cross border payment automation in 2026 will be comprehensive, but not opaque. AI systems will execute autonomously while maintaining full auditability and governance.

Key characteristics will include:

• Explainable AI decision logs for compliance and audit

• Configurable risk and approval thresholds

• Continuous learning from payment outcomes

This balance between autonomy and control will be critical for regulated industries and global enterprises operating at scale.

Real-Time Cash Intelligence for Treasury

Treasury teams will experience one of the biggest transformations. In 2026, AI will deliver forward-looking cash intelligence, not just visibility.

AI-driven treasury capabilities will include:

• Predictive cash positioning by currency and region

• Scenario modeling tied to payment and collection behavior

• Early warnings for liquidity stress

By tightly integrating cross-border payments into the customer-to-cash journey, AI will turn treasury into a proactive growth enabler.

What Finance Leaders Should Prepare for Now

The shift coming in 2026 is structural, not incremental. To stay ahead, finance leaders should assess whether their current infrastructure can support:

• Autonomous cross-border payments optimization

• AI-driven risk and credit decisioning

• Scalable bulk payments cross border and batch execution

• Intelligent cross border multi currency payment strategies

• End-to-end, explainable cross border payment automation

Systems built for visibility alone will struggle in a world that demands prediction and execution.

Final Thoughts

2026 will redefine how money moves across borders and how value is captured across the customer-to-cash journey. AI will no longer sit alongside finance operations - it will sit at the center of them.

Organizations that embrace AI-driven cross-border B2B payments will unlock faster cash cycles, lower risk, and superior customer experiences. Those that delay will find themselves constrained by systems designed for a world that no longer exists.

The future of customer-to-cash is intelligent, autonomous, and global - and 2026 is where it becomes real.