The Complete Guide to Customer-to-Cash in 2026

From buyer onboarding to cash collection — how AI is transforming every stage of the customer-to-cash lifecycle for modern B2B teams.

If you're running a B2B business that sells on credit — whether you're a wholesaler, distributor, manufacturer, or ecommerce platform — you already manage a customer-to-cash process. You just might not call it that.

Customer-to-cash (C2C) is the full journey from the moment a buyer enters your world to the moment their payment hits your bank account. It sounds simple. In practice, it's where most B2B companies leak money, time, and relationships without realizing it.

This guide breaks down everything you need to know about customer-to-cash in 2026: what it is, why it matters more than ever, how it differs from order-to-cash, and how leading companies are using AI to transform every stage of the journey.

The Customer-to-Cash Lifecycle

Customer-to-cash is the end-to-end process of converting a customer relationship into collected revenue. It encompasses every touchpoint between a buyer's first interaction and the final payment reconciliation.

The full C2C lifecycle includes seven stages:

1. Buyer Discovery & Onboarding — Who is this buyer? Are they legitimate? Can they pay? This stage covers KYB (Know Your Business) verification, identity checks, and initial credit assessment.

2. Credit Evaluation & Limit Setting — Assessing buyer creditworthiness and setting appropriate limits. This isn't a one-time gate — it's an ongoing process that should adapt to buyer behavior and market conditions.

3. Sales & Order Management — Quote generation, payment terms negotiation, order confirmation, and fulfillment. The terms agreed here directly determine how long it takes to collect.

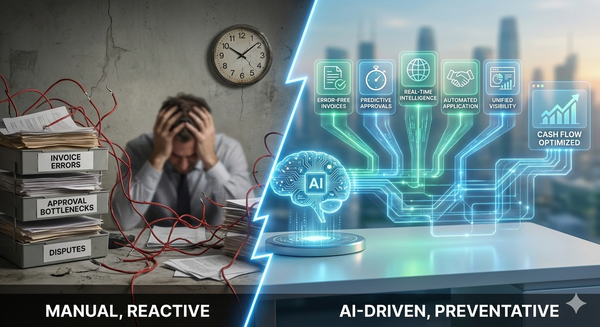

4. Invoicing — Invoice generation, validation, and delivery. Invoice accuracy is the single biggest controllable factor in payment speed.

5. Payment Collection — Payment method facilitation, dunning workflows, and cross-border payment processing. This is where AI is making the biggest impact today.

6. Reconciliation & Cash Application — Matching payments to invoices, handling exceptions, and confirming cash in bank. The most overlooked bottleneck in the entire cycle.

7. Analytics & Optimization — DSO tracking, buyer behavior analysis, cash flow forecasting, and continuous improvement.

Most companies manage these stages in silos. Buyer onboarding sits with sales and compliance. Invoicing is operations. Collection is finance. Reconciliation is accounting.

The result? Information doesn't flow. Problems in stage 1 create costs in stage 5. A bad credit decision at onboarding becomes a write-off at collection. A pricing error in the invoice becomes a 30-day dispute.

Customer-to-cash is the recognition that these aren't separate processes — they're one journey.

Customer-to-Cash vs. Order-to-Cash

You've probably heard of "order to cash" (O2C). It's the established term, used by most enterprise software vendors and finance teams. So why "customer to cash"?

The distinction matters.

Order-to-cash starts at the order. It assumes you already know who the buyer is, that credit has been approved, and that terms are set. O2C is a back-office operations process: order → invoice → collection → reconciliation.

Customer-to-cash starts at the customer. It includes everything O2C covers, but adds the critical upstream stages: buyer identification, credit assessment, risk monitoring, and relationship management.

In a world where trade is increasingly global, payment terms are extending, and buyer risk profiles shift rapidly, the upstream stages — buyer intelligence, credit management, risk monitoring — are where the real value is.

O2C optimizes the machine. C2C optimizes the outcome.

Why Customer-to-Cash Matters More in 2026

Three macro trends are making C2C optimization critical:

Payment terms are extending. Net-30 is becoming net-45. Net-60 is the norm in many industries. Some sectors routinely operate at net-90 or beyond. Buyers are quietly turning suppliers into their bank, and every additional day of DSO costs real money — approximately $27,400 per day for every $100M in annual revenue.

Global trade is getting more complex. Tariff uncertainty, regulatory shifts, currency volatility, and supply chain reorganization mean buyer risk profiles change faster than traditional credit assessment cycles can track. A buyer who was low-risk in January might be high-risk by March.

AI is rewriting the playbook. AI agents can now verify buyer identity in minutes, monitor buyer health continuously, automate personalized collection workflows, reconcile payments in real time, and forecast cash flow with accuracy that manual processes can't match. This isn't incremental improvement — it's a fundamental shift in what's possible for mid-market companies.

Stage 1: Buyer Intelligence & Onboarding

Most companies treat buyer onboarding as a binary gate — approve or reject — based on limited data and manual review. The process is slow (3-7 days is typical), which costs deals. And once a buyer is approved, their credit profile is rarely reassessed until something goes wrong.

What good looks like:

• Automated KYB verification that checks business registration, ownership, sanctions lists, and adverse media in minutes

• AI-driven credit scoring that synthesizes traditional bureau data with real-time signals — industry health, payment behaviors, market conditions

• Dynamic credit limits that adjust automatically based on buyer behavior and risk changes

• Continuous monitoring — not just a one-time check, but ongoing surveillance of financial, behavioral, and market indicators

Companies implementing automated buyer intelligence report 20-30% higher approval rates (because better data creates more confidence) while simultaneously reducing write-offs by 50-90%.

The tradeoff between buyer onboarding speed and risk mitigation is one of the most consequential decisions in the C2C cycle.

Stage 2: Credit Management & Terms

Sales teams negotiate payment terms without visibility into credit implications. Finance teams set rigid policies that lose deals. Neither team has the data to optimize the tradeoff.

What good looks like:

• Data-driven terms negotiation where sales can see a buyer's risk profile and recommended terms in their CRM

• Dynamic pricing for terms — longer terms cost more, early payment earns discounts, and pricing reflects actual cost of capital

• Portfolio-level optimization that balances growth and risk across the entire buyer base

The hidden costs of manual credit checks go far beyond the direct labor. They include missed opportunities from slow approvals, inconsistent decisions that create portfolio risk, and the inability to scale credit management as transaction volumes grow.

Stage 3: Invoicing & Accuracy

Invoice errors are the #1 cause of payment delays that companies can directly control. Wrong amounts, wrong references, wrong tax calculations — each error adds 15-30 days to collection time.

What good looks like:

• Automated invoice generation triggered by order fulfillment

• Validation rules that catch errors before the invoice goes out — price mismatches, duplicates, missing PO numbers

• Multi-channel delivery — email, portal, EDI, embedded in buyer's procurement system

• Multi-currency invoicing with automatic FX rate application

Every 1% reduction in invoice error rate translates to measurable DSO improvement. Companies that achieve less than 2% invoice error rates typically see DSO 10-15 days lower than their industry average.

Stage 4: Payment Collection

Manual collection doesn't scale. When one collector manages 200+ accounts, follow-ups become reactive — chasing accounts that are already past due instead of proactively managing those about to become past due.

What good looks like:

• AI-driven dunning that personalizes timing, channel, and messaging based on each buyer's behavior patterns

• Predictive prioritization that focuses human attention on accounts with the highest risk and highest value

• Multi-channel communication — email, phone, portal, SMS — orchestrated automatically

• Self-service payment portals where buyers can view invoices, raise queries, and pay without friction

AI-driven collection workflows typically reduce DSO by 15-30% and reduce manual collection activity by 50-70%. The top reasons for late payments are surprisingly consistent — and surprisingly fixable with the right automation.

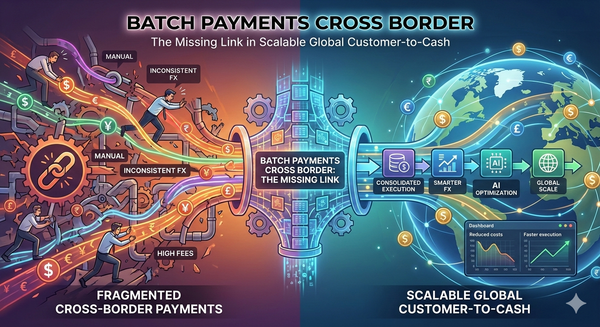

Stage 5: Cross-Border Payment Facilitation

For companies in global trade, payment collection has an additional layer of complexity. Cross-border payments involve FX risk, intermediary bank fees, longer settlement times, and compliance requirements.

What good looks like:

• Multi-currency acceptance — let buyers pay in their local currency

• Local payment rails — SEPA, Faster Payments, PIX — routed through the most efficient path

• Real-time FX conversion at competitive rates, not bank markups

• Automated compliance and documentation for each payment corridor

The companies getting this right aren't just saving on payment costs. They're removing friction that causes buyers to delay payments. When paying you is easy, buyers pay faster.

Stage 6: Reconciliation & Cash Application

This is the most overlooked stage — and often the most expensive. When a cross-border payment arrives with truncated references, incorrect amounts, different currencies, and no identifying information, someone has to figure out which invoice it belongs to.

What good looks like:

• AI-powered matching that identifies payment-invoice relationships even with incomplete data

• Real-time processing — payments matched as they arrive, not in weekly batches

• Automated exception handling for partial payments, overpayments, and FX differences

• Human-in-the-loop for genuine exceptions — the 5% that AI can't resolve gets routed to a specialist with full context

Automated cash application reduces reconciliation time by 80%+ and eliminates the "cash in bank but not applied" problem that distorts AR aging reports.

Stage 7: Analytics & Continuous Optimization

Most companies report on AR metrics retrospectively. By the time quarterly DSO reports are reviewed, the opportunity to act has passed.

What good looks like:

• Real-time dashboards showing DSO, aging, collection rates, and cash position by segment

• Predictive analytics forecasting cash flow based on historical patterns and current pipeline

• Buyer-level insights — understanding payment behavior at the individual account level

• Benchmarking against industry and peer performance

Building Your Customer-to-Cash Strategy

Not every stage needs immediate attention. Focus on the one that creates the most value:

• High write-offs? → Start with Stage 1 (Buyer Intelligence)

• High DSO? → Start with Stage 4 (Collection) or Stage 3 (Invoicing accuracy)

• Slow onboarding losing deals? → Start with Stage 1 (automated KYB)

• Reconciliation eating staff time? → Start with Stage 6 (Cash Application)

• No visibility into performance? → Start with Stage 7 (Analytics)

A practical implementation timeline:

Month 1-2: Connect your data. Get invoices, payments, and buyer information flowing into a single system.

Month 3-4: Automate reconciliation and cash application. Immediate ROI, low risk, builds confidence.

Month 5-6: Deploy AI-driven collection workflows. Start with your highest-volume accounts.

Month 7-9: Implement buyer intelligence and continuous monitoring. This is where the strategic value kicks in.

Month 10-12: Optimize terms, pricing, and credit policies based on accumulated data.

The Future of Customer-to-Cash

Three developments will define C2C over the next 2-3 years:

Agentic AI becomes standard. AI agents that make judgment calls — adjusting credit limits, negotiating payment plans, resolving disputes — will become the norm. The human role shifts from execution to oversight.

Real-time payments reshape expectations. As real-time payment rails expand globally, the expectation of instant settlement will push B2B toward faster payment cycles.

Embedded finance blurs the lines. C2C capabilities will embed directly into ecommerce platforms, ERPs, and marketplaces — making sophisticated financial operations accessible to businesses of every size.

Getting Started

The customer-to-cash journey is exactly that — a journey. You don't need to transform overnight. Start by understanding where your money leaks, pick the biggest lever, and build from there.

The companies that figure this out aren't just collecting faster. They're selling more confidently, managing risk more intelligently, and building competitive advantages that compound over time.

The cash was always there. The question is how fast, how safely, and how intelligently you convert it.

Ready to evaluate your customer-to-cash process? Use the ROI Calculator to quantify the impact of optimizing your C2C lifecycle — or explore our guides for actionable frameworks.