Top 5 Reasons for Late Payments – And How AI Fixes Them

Late payments are a systems problem, not a collections problem. Here's how AI-driven customer-to-cash platforms prevent them.

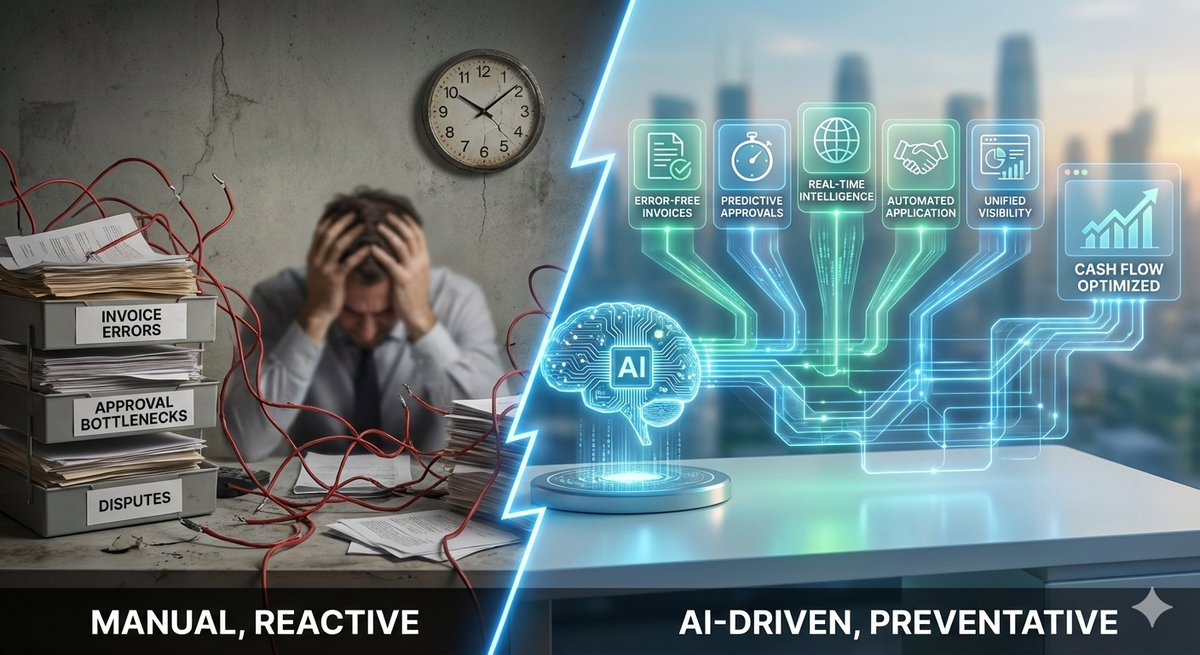

Late payments are often treated as a collections problem. But in most organizations, they are a systems problem.

Before escalating emails, tightening credit terms, or blaming customers, finance leaders should ask a more important question:

What inside our customer-to-cash process is contributing to late payments?

Research from Atradius, Dun & Bradstreet, and PwC consistently shows that the majority of late payments in B2B environments are not caused by insolvency. They are caused by process friction, disputes, administrative gaps, and poor visibility.

Here are the top five reasons for late payments – and how AI-driven customer-to-cash platforms are addressing them.

1. Invoice Errors and Disputes

One of the most common causes of late payments is simple: invoices are wrong or incomplete.

Common issues include:

• Pricing mismatches

• Incorrect tax calculations

• Missing purchase order numbers

• Inconsistent payment terms

• Delivery or quantity discrepancies

According to industry surveys, disputes contribute to 20–30% of delayed B2B payments.

How AI Helps

AI reduces invoice-related delays by:

• Validating invoice data before issuance

• Matching invoices automatically to contracts and purchase orders

• Flagging anomalies in pricing or quantities

• Predicting which invoices are likely to be disputed

Instead of reacting to disputes, AI prevents them.

2. Manual Approval Bottlenecks on the Buyer Side

Even when invoices are accurate, many buyers operate with layered approval workflows. If an invoice gets stuck internally, payment timing slips.

This is especially common in:

• Large enterprises with multi-step approvals

• Cross-border transactions

• Multi-entity organizations

Often, the seller has no visibility into where the delay is happening.

How AI Helps

AI improves approval visibility and timing by:

• Analyzing historical buyer payment behavior

• Identifying patterns in approval delays

• Triggering proactive reminders before due dates

• Recommending optimal invoice timing based on buyer behavior

By predicting delay risk, finance teams can intervene early rather than chase payments after they are overdue.

3. Cash Flow Constraints at the Buyer

Sometimes customers pay late not because they refuse to pay, but because they are managing their own working capital pressures.

In volatile markets, buyers may:

• Prioritize certain suppliers

• Stretch payment terms selectively

• Delay cross-border payments due to FX exposure

Late payment, in these cases, is a liquidity management decision.

How AI Helps

AI-driven buyer intelligence can:

• Detect early warning signs of financial stress

• Monitor payment pattern changes in real time

• Adjust credit limits dynamically

• Recommend payment plan or term adjustments proactively

Instead of escalating, finance teams can adapt intelligently and protect both revenue and relationships.

4. Poor Cash Application and Reconciliation

In some cases, the customer has paid – but the payment is not matched correctly.

Unapplied cash is a hidden contributor to perceived late payments.

Industry benchmarks from APQC show that organizations with high manual cash application rates experience significantly longer resolution times and increased DSO.

How AI Helps

AI-powered cash application:

• Automatically matches payments to invoices

• Identifies short pays and deductions

• Learns from historical matching patterns

• Resolves exceptions without manual intervention

This reduces artificial aging and prevents unnecessary collection efforts.

5. Fragmented Ownership Across the Customer-to-Cash Process

Late payments often reflect internal silos:

• Sales negotiates terms

• Finance issues invoices

• Treasury manages receipts

• Collections chase balances

Without unified visibility, small gaps become systemic delays. When no one owns end-to-end cash velocity, inefficiencies accumulate.

How AI Helps

AI-driven customer-to-cash platforms unify data across:

• Credit

• Invoicing

• Payments

• FX

• Collections

• Cash application

This creates a single, predictive view of payment risk and timing. Instead of reacting to overdue invoices, finance teams operate with forward-looking insight.

Late Payments in Customer-to-Cash Are Usually Predictable

One of the biggest misconceptions in B2B finance is that late payments are random.

In reality, they are highly predictable when you analyze:

• Buyer behavior

• Invoice characteristics

• Payment methods

• Country risk

• Internal processing patterns

AI thrives on these signals.

Organizations using predictive analytics in order-to-cash consistently report measurable improvements in DSO, reduced disputes, and lower collection effort.

The Strategic Shift: From Collections to Prevention

The real shift is moving from collections to prevention.

Instead of asking:

"Why is this invoice overdue?"

Leading finance teams ask:

"Which invoices are likely to be late, and what can we do before that happens?"

That mindset change – powered by AI – transforms late payments from a reactive problem into a manageable variable.

Late payments are rarely just about customer intent. They are usually the result of invoice friction, approval bottlenecks, liquidity pressures, reconciliation gaps, or fragmented systems.

AI does not replace collections teams. It empowers them.

By embedding intelligence across the customer-to-cash journey, organizations can reduce late payments, improve cash flow, and strengthen customer relationships at the same time.

The future of order-to-cash is not louder reminders.

It is smarter prevention.

Is your current customer-to-cash system predicting late payments – or merely reacting to them? Explore the ROI Calculator to see the impact of AI-driven prevention on your cash flow.